Opinion on financial statements of Bodycote plc

Opinion

In our opinion:

- the financial statements give a true and fair view of the state of the Group's and of the Parent Company's affairs as at 31 December 2017 and of the group's profit for the year then ended;

- the Group financial statements have been properly prepared in accordance with International Financial Reporting Standards (IFRSs) as adopted by the European Union;

- the Parent Company Financial statements have been properly prepared in accordance with United Kingdom Generally Accepted Accounting Practice including Financial Reporting Standard 101 "Reduced Disclosure Framework" and;

- the financial statements have been prepared in accordance with the requirements of the Companies Act 2006 and, as regards the Group financial statements, Article 4 of the IAS Regulation.

We have audited the financial statements of Bodycote plc (the 'Parent Company') and its subsidiaries (the 'Group') which comprise:

- the Consolidated Income Statement;

- the Consolidated Statement of Comprehensive Income;

- the Consolidated and Parent Company Statements of Financial Position;

- the Consolidated Cash Flow Statement;

- the Consolidated and Parent Company Statements of Changes in Equity;

- the Group and Company Accounting Policies;

- the related notes 1 to 29 to the Group financial statements; and

- the relates notes 1 to 12 to the Parent Company financial statements.

The financial reporting framework that has been applied in the preparation of the Group financial statements is applicable law and IFRSs as adopted by the European Union. The financial reporting framework that has been applied in the preparation of the Parent Company financial statements is applicable law and United Kingdom Accounting Standards, including FRS 101 "Reduced Disclosure Framework" (United Kingdom Generally Accepted Accounting Practice).

Basis for opinion

We conducted our audit in accordance with International Standards on Auditing (UK) (ISAs (UK)) and applicable law. Our responsibilities under those standards are further described in the auditor's responsibilities for the audit of the financial statements section of our report.

We are independent of the Group and the Parent Company in accordance with the ethical requirements that are relevant to our audit of the financial statements in the UK, including the FRC's Ethical Standard as applied to listed public interest entities, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We confirm that the non-audit services prohibited by the FRC's Ethical Standard were not provided to the Group or the Parent Company.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Summary of our audit approach

Key audit matters | The key audit matters that we identified in the current year were: - Impairment of goodwill and intangible fixed assets in Europe ST

- Taxation accounting – valuation of certain tax structure provisions

- Pensions – UK defined benefit scheme liability assumptions

- Revenue recognition – manual adjustments to revenue

Within this report, any new key audit matters are identified with  and any key audit matters which are the same as the prior year identified with and any key audit matters which are the same as the prior year identified with  . . |

Materiality | The materiality that we used for the group financial statements was £5.6 million which was determined on the basis of 5% of expected pre-tax profit. |

Scoping | As a consequence of the audit scope determined, we achieved coverage of approximately 73% of revenue, 78% of profit before tax and 79% of net assets. |

Significant changes in our approach | Our approach is consistent with the previous year with the exception of the removal of the completeness and accuracy of environmental provisions as a key audit matter for the 2017 audit report, and the addition of the potential fraud risk in relation to revenue recognition, as outlined in further detail below. |

Conclusions relating to going concern, principal risks and viability statement

Going concern |

- We have reviewed the directors' statement in the Chief Financial Officer's Report to the financial statements about whether they considered it appropriate to adopt the going concern basis of accounting in preparing them and their identification of any material uncertainties to the group's and company's ability to continue to do so over a period of at least twelve months from the date of approval of the financial statements.

- We are required to state whether we have anything material to add or draw attention to in relation to that statement required by Listing Rule 9.8.6R(3) and report if the statement is materially inconsistent with our knowledge obtained in the audit.

| We confirm that we have nothing material to report, add or draw attention to in respect of these matters. |

Principal risks and viability statement |

Based solely on reading the directors' statements and considering whether they were consistent with the knowledge we obtained in the course of the audit, including the knowledge obtained in the evaluation of the directors' assessment of the Group's and the Company's ability to continue as a going concern, we are required to state whether we have anything material to add or draw attention to in relation to: - the disclosures in the Principal risks and uncertainties that describe the principal risks and explain how they are being managed or mitigated;

- the directors' confirmation in the Directors' responsibilities statement that they have carried out a robust assessment of the principal risks facing the group, including those that would threaten its business model, future performance, solvency or liquidity; or

- the directors' explanation in the Chief Financial Officer's report as to how they have assessed the prospects of the Group, over what period they have done so and why they consider that period to be appropriate, and their statement as to whether they have a reasonable expectation that the Group will be able to continue in operation and meet its liabilities as they fall due over the period of their assessment, including any related disclosures drawing attention to any necessary qualifications or assumptions.

We are also required to report whether the directors' statement relating to the prospects of the Group required by Listing Rule 9.8.6R(3) is materially inconsistent with our knowledge obtained in the audit. | We confirm that we have nothing material to report, add or draw attention to in respect of these matters. |

Key audit matters |

Key audit matters are those matters that, in our professional judgement, were of most significance in our audit of the financial statements of the current period and include the most significant assessed risks of material misstatement (whether or not due to fraud) that we identified. These matters included those which had the greatest effect on: the overall audit strategy, the allocation of resources in the audit; and directing the efforts of the engagement team. These matters were addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters. In 2017 we no longer consider the completeness and accuracy of environmental remediation provisions to be a key audit matter. This assessment is based on the stable nature of the site portfolio and associated environmental obligations across the Group, and support provided by third-party environmental specialist valuation reports. We have included a new key audit matter for 2017 in relation to the fraud risk in revenue recognition, focused on the risk of manual adjustments made to revenue, which has been included following consideration of the nature of revenue transactions recorded by the Group and the typical sales cycle for services provided, as described further within the Key Audit Matter below. We have also refined our key audit matter in relation to impairment to focus on intangible fixed assets (including goodwill) balances for the Europe ST cash generating unit ("CGU"), as opposed to tangible and intangible fixed assets across the whole business. |

Impairment of intangible fixed assets (including goodwill)

Key audit matter description  | The Group has a significant non-current asset base relating to intangible assets (including goodwill) of £201.0m (2016: £206.7m) as shown in notes 11 and 12. Our risk assessment procedures have pinpointed our key audit matter with regards to impairment to focus on the Europe ST CGU (which has £12.6m of goodwill allocated (2016: £12.6m)), due to the continued adverse performance related to the oil and gas markets served by this CGU. Performing an impairment review of the non-current assets within this CGU requires the exercise of judgement regarding future growth rates, discount rates and sensitivity assumptions, as described in note 11, and is included as an area of focus in the Report of the Audit Committee. |

How the scope of our audit responded to the key audit matter  | We challenged the assumptions used in the impairment model for intangible assets within the Europe ST CGU. As part of our procedures we: - We challenged the assumptions used in the impairment model for intangible assets within the Europe ST CGU. As part of our procedures we:

- considered the appropriateness of the growth rate assumptions by comparing them to historical trading performance and World Bank historical GDP data for the markets served by Europe ST, and reviewing and challenging management's budget for 2018;

- considered the impact of the sensitivities performed by management in assessing whether they reflect a reasonable possible change scenario; and

- assessed the appropriateness of the assumptions concerning the discount rate applied by engaging our internal valuation specialists to review the inputs used to determine the discount rate applied by comparing them against external market data.

|

Key observations  | Based on the procedures performed, no impairment was noted and we have concluded that the assumptions in the impairment model are appropriate. |

Taxation – valuation of certain tax structure provisions

Key audit matter description | The tax risk concerns the judgements and estimates applied in the determination of provisions for liabilities attributed to specific uncertain tax positions linked to the Group's corporate arrangements as described as an area of focus in the Report of the Audit Committee. |

How the scope of our audit responded to the key audit matter | In conjunction with our taxation audit specialists, we have assessed the assumptions and judgements concerning the adequacy of certain tax structure provisions by challenging management's assumptions, reviewing the available correspondence from the various tax authorities and drawing on the experience of our taxation specialists in respect of similar situations. |

Key observations | From the work performed above we are satisfied that the provisions held on the balance sheet for certain tax structure positions are reasonable. |

Pensions – UK defined benefit scheme liability assumptions

Key audit matter description | This risk concerns the appropriateness of the actuarial assumptions applied in calculating the Group's UK defined benefit scheme liability of £109.9m (2016: £126.6m) within the net UK defined benefit surplus of £2.4m (2016: liability of £3.6m) as shown in note 28. The valuation of the Group's IAS 19 liability involves significant judgement in the choice of discount rate used and in the key sources of estimation uncertainty in particular in relation to the discount rate assumptions, as described in the Group's accounting policies, and is included as an area of focus in the Report of the Audit Committee. |

How the scope of our audit responded to the key audit matter | We have assessed the appropriateness of the assumptions underpinning the valuation of the scheme liabilities. Specifically we challenged the discount rate, inflation and mortality assumptions applied in the calculation by using our internal pension specialists to benchmark the assumptions applied against comparable third party data and assessed the appropriateness of the assumptions in the context of the Group's own position. |

Key observations | From the work performed we are satisfied that the assumptions applied in respect of the valuation of the Group's IAS 19 UK defined benefit scheme liabilities are reasonable. We consider the assumptions to be towards the prudent end of our benchmarked range. |

Revenue recognition - manual adjustments to revenue

Key audit matter description | When assessing the potential risk of fraud in relation to revenue recognition, we have considered the nature of the automated and manual transactions recorded across the Group, considering the typical sales cycle for the services provided by the Group as described in the Group's accounting policies, and have determined that the key audit matter in relation to fraud is pinpointed to the risk of inappropriate manual adjustments being recorded in revenue. |

How the scope of our audit responded to the key audit matter | We have profiled the population of journal entries made throughout the year in order to identify manual adjustments made to revenue and have tested the identified population to validate their authenticity and commercial substance. |

Key observations | From the work performed we have not noted any manual adjustments to revenue that we would not expect in the usual course of business, or that cannot be supported. |

Our application of materiality

We define materiality as the magnitude of misstatement in the financial statements that makes it probable that the economic decisions of a reasonably knowledgeable person would be changed or influenced. We use materiality both in planning the scope of our audit work and in evaluating the results of our work.

Based on our professional judgement, we determined materiality for the financial statements as a whole as follows:

| Group financial statements | Parent company financial statements |

| Group materiality | £5.6 million (2016: £4.8 million) | £4.5 million (2016: £3.6 million) |

| Basis for determining materiality | 5% of expected pre-tax profit (2016: 5% of pre-tax profit) | The parent company materiality represents 1% (2016: 1%) of equity which is capped at 80% (2016: 80%) of Group materiality. |

| Rationale for the benchmark applied | Pre-tax profit is determined to be the most stable basis of underlying business performance. | As a non-trading parent company, equity is the key driver of the company. |

We agreed with the Audit Committee that we would report to the Committee all audit differences in excess of £0.28 million (2016: £0.20 million) for the group, as well as differences below that threshold that, in our view, warranted reporting on qualitative grounds. We also report to the Audit Committee on disclosure matters that we identified when assessing the overall presentation of the financial statements.

An overview of the scope of our audit

Our Group audit was scoped by obtaining an understanding of the Group and its environment, including group-wide controls, and assessing the risks of material misstatement at the Group level.

Based on this assessment, we focused our Group audit scope primarily on the audit work relating to twelve components across nine core locations, being USA, UK, France, Germany, Sweden, the Netherlands, Czech Republic, Turkey, and Mexico. Components within China, Italy and Poland were removed from Group scope as part of our risk assessment process to pinpoint our focus and attention to material components where the key audit matters and judgements affecting the Group financial statements are expected. The parent company is located in the UK and audited directly by the Group audit team.

As a consequence of the audit scope determined, we achieved coverage of approximately 73% (2016: 86%) of revenue, 78% (2016: 92%) of profit before tax and 79% (2016: 90%) of net assets. Our audit work at each location was executed at levels of materiality applicable to each individual entity which were lower than Group materiality. Component materiality, excluding the Parent Company, ranged from £1.5m to £2.8m (2016: £0.5m to £2.5m).

The Group audit team continued to follow a program of planned visits that has been designed so that a senior member of the Group audit team visits each of the significant finance function locations included as full scope for the Group audit at least once every three years. During the year, senior members of the Group audit team have visited the US, UK, France and the Czech Shared Service Centre.

In years when we do not visit a significant component we include the component audit team in our team briefing, discuss their risk assessment, attend close meetings by conference call and review documentation of the findings from their work.

At the parent entity level we also tested the consolidation process and carried out analytical procedures to confirm our conclusion that there were no significant risks of material misstatement of the aggregated financial information of the remaining components not subject to audit or audit of specified account balances.

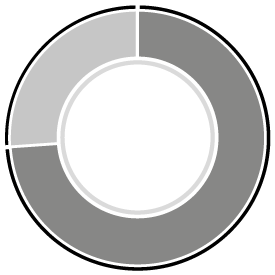

Revenue

- Full audit scope 73%

- Review at Group level 26%

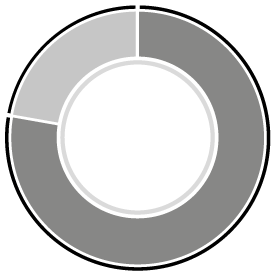

Profit before tax

- Full audit scope 78%

- Review at group level 22%

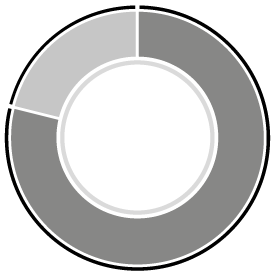

Net assets

- Full at scope 79%

- Review at Group level 21%

Other information

The directors are responsible for the other information. The other information comprises the information included in the annual report, other than the financial statements and our auditor's report thereon. Our opinion on the financial statements does not cover the other information and, except to the extent otherwise explicitly stated in our report, we do not express any form of assurance conclusion thereon. In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If we identify such material inconsistencies or apparent material misstatements, we are required to determine whether there is a material misstatement in the financial statements or a material misstatement of the other information. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. In this context, matters that we are specifically required to report to you as uncorrected material misstatements of the other information include where we conclude that: - Fair, balanced and understandable – the statement given by the directors that they consider the annual report and financial statements taken as a whole is fair, balanced and understandable and provides the information necessary for shareholders to assess the group's position and performance, business model and strategy, is materially inconsistent with our knowledge obtained in the audit; or

- Audit committee reporting – the section describing the work of the audit committee does not appropriately address matters communicated by us to the audit committee; or

- Directors' statement of compliance with the UK Corporate Governance Code – the parts of the directors' statement required under the Listing Rules relating to the company's compliance with the UK Corporate Governance Code containing provisions specified for review by the auditor in accordance with Listing Rule 9.8.10R (2) do not properly disclose a departure from a relevant provision of the UK Corporate Governance Code.

| We have nothing to report in respect of these matters. |

Responsibilities of directors

As explained more fully in the directors' responsibilities statement, the directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view, and for such internal control as the directors determine is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, the directors are responsible for assessing the group's and the parent company's ability to continue as a going concern, disclosing as applicable, matters related to going concern and using the going concern basis of accounting unless the directors either intend to liquidate the group or the parent company or to cease operations, or have no realistic alternative but to do so.

Auditor's responsibilities for the audit of the financial statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with ISAs (UK) will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

A further description of our responsibilities for the audit of the financial statements is located on the Financial Reporting Council's website at: www.frc.org.uk/auditorsresponsibilities. This description forms part of our auditor's report.

Use of our report

This report is made solely to the company's members, as a body, in accordance with Chapter 3 of Part 16 of the Companies Act 2006. Our audit work has been undertaken so that we might state to the company's members those matters we are required to state to them in an auditor's report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the company and the company's members as a body, for our audit work, for this report, or for the opinions we have formed.

Report on other legal and regulatory requirements

Opinions on other matters prescribed by the Companies Act 2006

In our opinion the part of the directors' remuneration report to be audited has been properly prepared in accordance with the Companies Act 2006.

In our opinion, based on the work undertaken in the course of the audit:

- the information given in the strategic report and the directors' report for the financial year for which the financial statements are prepared is consistent with the financial statements; and

- the strategic report and the directors' report have been prepared in accordance with applicable legal requirements.

In the light of the knowledge and understanding of the group and of the parent company and their environment obtained in the course of the audit, we have not identified any material misstatements in the strategic report or the directors' report.

Matters on which we are required to report by exception

Adequacy of explanations received and accounting records |

Under the Companies Act 2006 we are required to report to you if, in our opinion: - we have not received all the information and explanations we require for our audit; or

- adequate accounting records have not been kept by the parent company, or returns adequate for our audit have not been received from branches not visited by us; or

- the parent company financial statements are not in agreement with the accounting records and returns.

| We have nothing to report in respect of these matters. |

Directors' remuneration |

Under the Companies Act 2006 we are also required to report if in our opinion certain disclosures of directors' remuneration have not been made or the part of the directors' remuneration report to be audited is not in agreement with the accounting records and returns. | We have nothing to report in respect of these matters. |

Other matters

Auditor tenure

Following the recommendation of the audit committee, we were appointed by the Board of Directors in 2002 to audit the financial statements for the year ending 31 December 2003 and subsequent financial periods. The period of total uninterrupted engagement including previous renewals and reappointments of the firm is 15 years, covering the years ending 31 December 2003 to 31 December 2017.

Consistency of the audit report with the additional report to the audit committee

An audit involves obtaining evidence about the amounts and disclosures in the financial statements sufficient to give reasonable assurance that the financial statements are free from material misstatement, whether caused by fraud or error. This includes an assessment of: whether the accounting policies are appropriate to the Group's and the Parent Company's circumstances and have been consistently applied and adequately disclosed; the reasonableness of significant accounting estimates made by the directors; and the overall presentation of the financial statements. In addition, we read all the financial and non-financial information in the Annual Report to identify material inconsistencies with the audited financial statements and to identify any information that is apparently materially incorrect based on, or materially inconsistent with, the knowledge acquired by us in the course of performing the audit. If we become aware of any apparent material misstatements or inconsistencies we consider the implications for our report.

Mark Mullins FCA (Senior statutory auditor)

for and on behalf of Deloitte LLP

Chartered Accountants and Statutory Auditor

London, United Kingdom

6 March 2018